Starting a business is a bold move, but what are the chances that you’ll succeed? Discover the average failure rates for U.S. businesses and what you can do to beat the odds.

Business ownership offers autonomy and the potential for high earnings, but success rarely comes fast or easy. Most entrepreneurs invest significant amounts of time, energy, and money into getting their ventures off the ground. Beyond identifying and satisfying a need in the market, they need to build brand awareness, develop operational systems, hire the right team, and much more. While it’s no easy feat, the stats show it’s possible. Read on to find out how often U.S. businesses fail and five ways to improve your chances of success.

What are the failure rates of U.S. businesses?

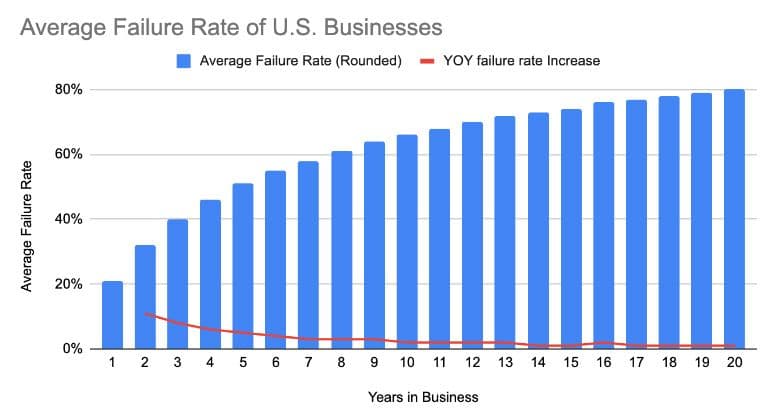

About one in five U.S. businesses (21%) fail in their first year, according to a BusinessLoans.com analysis of data from the U.S. Bureau of Labor Statistics (BLS). The good news is — if you make it past the first year, the odds of failing tend to decrease in each subsequent year. For example, while an average of 21% of businesses fail in year one, only an additional 11% fail in year two, 8% in year three, and 6% in year four. A downward or steady year-over-year trend continues through year 20 with only one exception.

Average business failure rates, 1994 to 2023

Four of five U.S. businesses survive their first year, but how many make it to year five, 10, and beyond? About half of businesses survive to the five-year mark, on average, while 34% make it 10 years and 20% make it to year 20. Here’s a closer look at the average failure rates by years in business, up to year 20, plus the year-over-year rate changes.

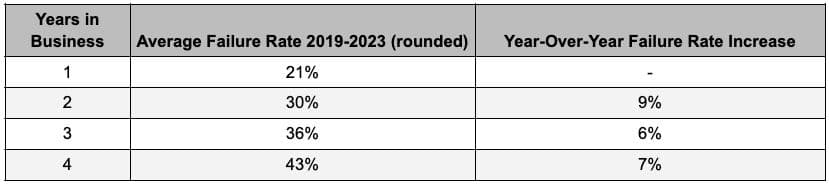

Average business failure rates, 2019 to 2023

The above stats provide average business failure rates based on 29 years of data, but what about the more recent years? While the COVID-19 pandemic and resulting economic problems caused many disruptions, business failure rates didn’t change much. When looking at companies founded between 2019 and 2023, the average failure rate after one year was still 21%, according to BLS data. In the following years, the failure rates were slightly lower than those from the larger data set; 30% after two years in business, 36% after three, and 43% after four.

Business survival rates by industry and location

If you’re looking for a more granular breakdown of business failure rates, you can look to the stats for your industry and state. For example, according to a 10-year BLS analysis of businesses started in 2013, companies in the following three industries had the highest 10-year survival rates:

- Agriculture, forestry, fishing, and hunting: 50.5%

- Utilities: 45.7%

- Manufacturing: 43.6%

On the other hand, businesses in the following three industries had the lowest 10-year survival rates:

- Wholesale trade: 32.1%

- Information: 29.1%

- Mining, quarrying, and oil and gas extraction: 24.5%

Additionally, there are notable differences in the survival rates of businesses in different states. For example, California’s 2023 one-year business survival rate was 81.5%, whereas Rhode Island’s was about 7% lower at 74.6%.

Tip: You can look up business survival stats for your industry and state with the BLS.

Is the overall number of U.S. businesses declining?

With a significant percentage of U.S. businesses shutting down each year, you may wonder if the net number of businesses in the U.S. is growing or declining. According to the SBA, there has been net annual growth every year since 2012, when the reported data starts. In 2020, the increase was the smallest of any reported year, but it was followed by a rebound in 2021 which was larger than any other reported year.

Why do businesses fail?

Businesses generally fail when their leaders decide that the costs associated with continuing operations outweigh the potential benefits — although there are some cases of closures by third parties (e.g. regulatory agencies). The former may be the case if a new business doesn’t generate enough revenue within a certain amount of time, or if a once-successful business experiences a steep downturn. Here’s a closer look at both scenarios and why they can occur.

New business failures

For a new business to be successful, it typically needs to solve a problem that impacts a sizeable segment of people, make the target audience aware of the solution, and convince them to try it. From there, the solution needs to be good enough that the customers are satisfied and become advocates for it.

Beyond the basics of product-market fit, effective sales and marketing, and building a loyal customer base, business owners have a variety of other responsibilities to manage. For example, they may need to handle pricing, inventory, accounting, staffing, employee management, loss prevention, customer service, and more. If anything goes awry, it could derail a new, vulnerable business.

Further, new businesses are often racing against the clock. They need to become profitable before their funding resources run out. Even if everything is going okay, failure can simply be the result of profitability not happening fast enough.

Established business failures

Once a business finds its footing and becomes profitable, it’s still not free from the risk of failure. The world is constantly changing and businesses have to adapt or risk losing ground. Blockbuster’s demise is a classic example of that.

Founded in 1985, the video rental store became an industry giant with more than 9,000 stores during its 2004 peak. However, it began to struggle when streaming and mailing platforms emerged, namely Netflix. The company had a “too big to fail” mindset and wasn’t proactive about adapting. It even reportedly passed on a chance to acquire Netflix for $50 million.

By 2009, Blockbuster posted a $500 million loss, was delisted from the New York Stock Exchange, and saw partners flee. In 2010, it filed for corporate bankruptcy. While the company could’ve gobbled up Netflix and transitioned into being the streaming leader, it’s hesitancy to evolve caused it to become a go-to case study on missed opportunities. Borders, the old book store chain, is another one.

Beyond the need to evolve and stay competitive, established businesses are also vulnerable to various threats. Their profitability can be disrupted by natural disasters, pandemics, economic downturns, disruptive leadership changes, lawsuits, bad PR, poor strategic decisions, regulatory changes, and more.

An example of a failure due to a pandemic and regulatory changes can be found in CommonBond’s story. The company launched in 2012 and became a successful student loan lender. Over 10 years, it funded more than $5 billion in loans, served over 100,000 customers, employed hundreds of people, and was named one of the 50 most innovative companies in the world by the Fast Company. So, what went wrong?

CommonBond founder, David Klein, says the company’s downfall began with the COVID-19 pandemic. The federal government paused student loan payments which took away half of the refinance market for several years. The lender tried to pivot into solar loans and was making progress, but couldn’t become profitable fast enough to save the business.

In some cases, unexpected events can pull the rug out from under a business, making it difficult to stay afloat. In others, it can be internal mistakes such as letting quality slide or failing to promptly respond to changes in the market.

How can you prevent business failure?

While succeeding as a business owner depends on a wide range of factors and a bit of good fortune, here are five steps that can help prevent failure:

- Assess the situation: Assess the time, money, and effort required to start the business. Research the market, talk to other business owners in your industry, write a business plan that includes costs and projections, perform a SWOT analysis, and scout talent. With a thorough understanding of what’s involved, explore why you want to start the business and be honest with yourself about whether you currently have the time, energy, and desire to see it through.

- Secure funding: Ensure you have adequate funding to start the business, cover all your personal living expenses, and keep the business running until it’s expected to be profitable (using conservative estimates). Identify how you will fund it, such as through your savings, investors, financing, or another funding source.

- Run lean: Consider starting with a lean operation and testing the market with small-scale experiments. You can limit risk by making decisions backed by evidence. If you want to launch a clothing line, for example, you could start by building your brand on social media and releasing individual items. From there, you could use the feedback to design your first drop. Then, you could build out your inventory based on what people buy most and, eventually, open a physical location. Taking this approach is much less risky than, say, starting with a physical location and stocking it full of inventory your theoretical target audience might want.

- Be proactive: Plan for the best but prepare for the worst. Handling problems and challenges is a normal part of running a business, so plan to continuously sniff out and prevent potential issues. When you inevitably encounter problems, look to not only resolve them but prevent them from happening again. Further, if you spot a new trend emerging or a shift coming, look for ways to embrace it and better serve your customers. Never get too comfortable. Even the biggest brands can fall fast if they fail to innovate.

- Seek mentorship: Join business communities, whether online or in person. Talk with other business owners and people in the industry, and seek advice from those who have done what you want to do. You may even want to hire a mentor. Connecting with the right people can fast-track your path to success and help you avoid pitfalls.

Building a business isn’t for the faint of heart. There is a very real possibility of failing and you will likely be faced with many challenging situations. However, the odds are technically in your favor for the first four years. And, if you play your cards right, you could very well start one of the businesses that stands the test of time.

Methodology: The data analysis for this article involved pulling the “business survival rates since birth” from March 1994 to March 2023 from a document published by the U.S. Bureau of Labor Statistics entitled, “Survival of private sector establishments by opening year.” The data set for each business birth year lists the survival rate for each subsequent year through March 2023. The average survival rate for each business year, 1 through 20, was found by adding together the survival rates for the given business year from each data set and dividing the sum by the total number of survival rates included. Average failure rates were then calculated by subtracting the average survival rates from 100.